📊 Full opportunity report: The $60 Billion Bargain: Why Cursor Could Be a Steal for SpaceX on ThorstenMeyerAI.com — validation score, market gap, and execution plan.

TL;DR

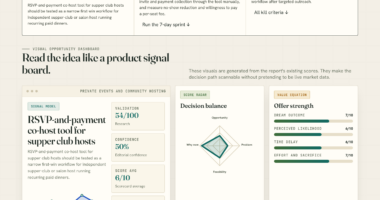

SpaceX exercised an option to acquire AI coding platform Cursor for $60 billion in stock, a move that analysts see as a strategic bargain due to Cursor’s rapid revenue growth and potential for integration. The deal is largely in SpaceX stock, with the market reacting positively.

The $60B bargain: why Cursor could be a steal

$60 billion for a code editor sounds like a bubble. Look past the headline and the price isn’t the scandal — it’s the discount. Here’s the case that SpaceX got Cursor cheap.

A melting multiple, paid in appreciating paper that cost almost nothing, for the profitable leader of the only AI category reliably making money — plus the missing app layer and an escape from the margin trap. If the growth holds and integration doesn’t break the product, $60B will read like a down payment. The risk isn’t overpaying for what Cursor is — it’s breaking what made it worth buying.

Strategic Implications of the Cursor Acquisition for SpaceX

This deal exemplifies a strategic move by SpaceX to vertically integrate AI capabilities, reducing reliance on external providers and potentially increasing profit margins. Acquiring Cursor not only accelerates SpaceX’s AI development but also denies key assets to competitors like OpenAI and Microsoft, consolidating its position in enterprise AI workflows. The deal’s structure, paid entirely in stock, highlights SpaceX’s high valuation and market confidence, enabling a significant asset acquisition with minimal immediate dilution. As AI becomes central to enterprise operations, owning a leading developer platform and proprietary models positions SpaceX to capitalize on future growth in AI-driven industries, extending its influence beyond aerospace into the broader tech ecosystem.AI coding platform subscription

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Background on SpaceX’s AI and Acquisition Strategy

Previously, Cursor was known for its rapid revenue growth and leadership in AI coding tools, with over a million paying users and a strong enterprise presence. It had turned down offers from OpenAI and Microsoft, indicating its strategic independence and value. The company had been squeezed by third-party API costs, which limited profitability despite revenue growth. SpaceX’s history of vertical integration, from rockets to satellites, suggests a pattern of acquiring key assets to control costs and accelerate development. The recent IPO valuation of SpaceX at over $2 trillion provided the financial capacity to make large acquisitions in stock, a tactic Musk has used before to fund strategic growth without immediate cash expenditure.“We are excited to integrate Cursor’s innovative AI tools into our ecosystem, accelerating our AI initiatives and strengthening our position in enterprise workflows.”

— SpaceX spokesperson

enterprise code editor software

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Uncertainties and Risks in the Acquisition

It is not yet clear how smoothly Cursor will integrate into SpaceX’s existing operations or how the company will manage potential cultural and technical challenges. The long-term profitability impact remains uncertain, especially as the AI market evolves rapidly. Additionally, the valuation assumptions, particularly regarding future revenue growth and margin expansion, are subject to market and technological risks that could alter the deal’s perceived value.developer AI tools

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Next Steps for SpaceX and Cursor Post-Acquisition

SpaceX is expected to begin integrating Cursor’s technology and team into its AI and software development efforts. The company will likely focus on internalizing AI costs and expanding Cursor’s enterprise reach. Monitoring Cursor’s revenue trajectory and profitability will be key, as well as observing how competitors respond to the consolidation. Further strategic moves or acquisitions may follow as SpaceX leverages this asset to enhance its AI capabilities and market position.AI programming IDE

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Key Questions

Why did SpaceX pay so much for Cursor?

SpaceX paid a high valuation due to Cursor’s rapid growth, strategic assets like its proprietary coding model, and its position as a leading AI developer platform with a profitable enterprise segment. The deal was structured in stock, taking advantage of SpaceX’s high market cap.What does this mean for competitors like OpenAI or Microsoft?

The acquisition denies these rivals access to Cursor’s developer platform and proprietary AI models, potentially giving SpaceX a competitive edge in enterprise AI workflows.How will SpaceX benefit financially from this deal?

By internalizing AI costs and owning a profitable AI platform, SpaceX could improve margins and accelerate AI-driven product development, creating long-term financial benefits.Is this acquisition risky for SpaceX?

While the strategic rationale is strong, integration challenges and market uncertainties remain. The long-term success depends on how well SpaceX can leverage Cursor’s technology and growth potential.Source: ThorstenMeyerAI.com